Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Economist: ‘Timing’ the Market May Not Work for Buyers

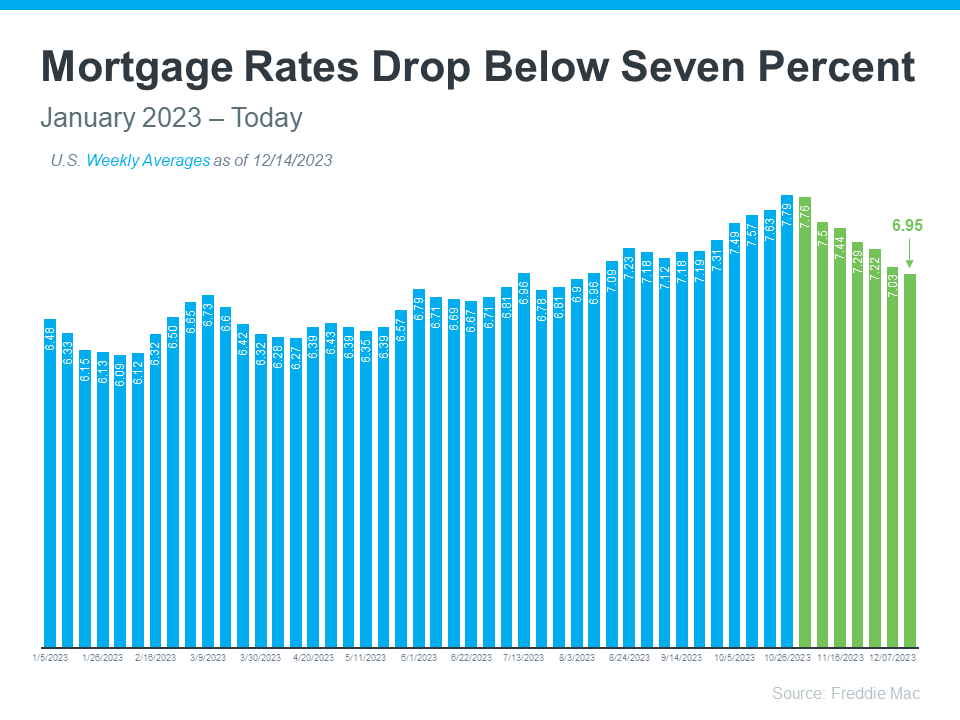

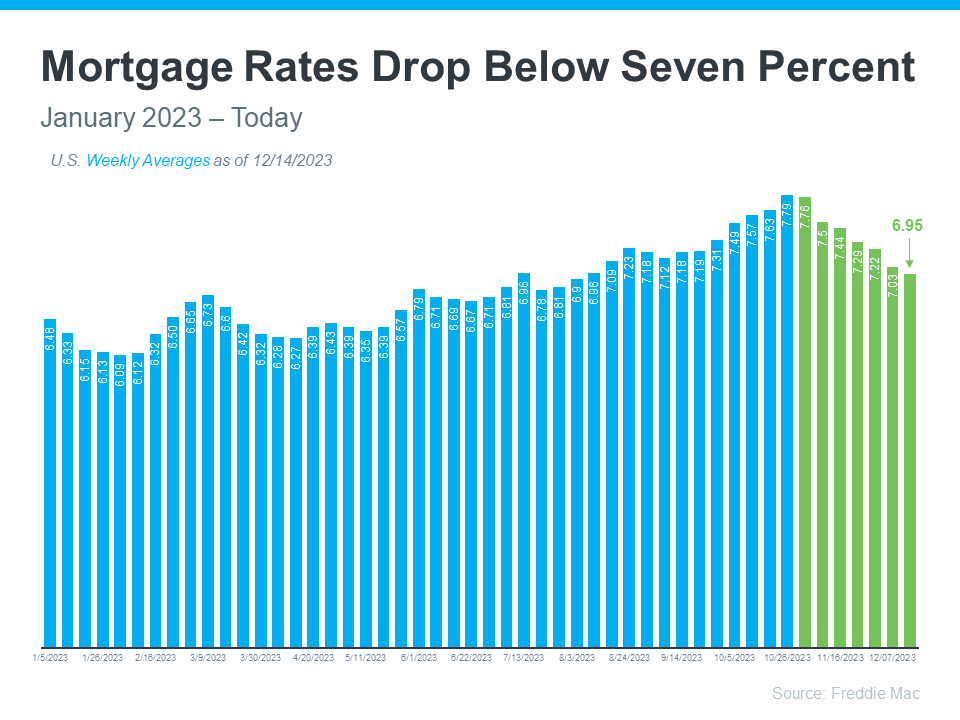

Home shoppers are sensitive to mortgage rates, which was made clear this week with an increase in the average for the 30-year fixed-rate mortgage. The rate rose to 6.77%, and mortgage applications for home purchases fell 3%, according to the Mortgage Bankers Association.

Every notch up and down in rates can impact home buyers’ purchasing power, but borrowing costs have largely stabilized. “While mortgage interest rates edged up weekly, the overall trajectory from fall 2023 is down and is now a full percentage point below the recent high” when rates neared 8%, says Jessica Lautz, deputy chief economist at the National Association of REALTORS®. “While mortgage interest rates may come down to the low 6% range in the middle to later part of the year, buyers must weigh what makes the most sense for them. Timing the real estate market based purely on mortgage interest rates—especially marginal changes—rarely works when new babies, marriages and jobs are the real decision-makers.”

Buyers may not save much by waiting, either. Home buyers purchasing the typical home at $400,000, with a 20% down payment, would likely have a monthly mortgage payment of about $2,080 at this week’s rate average, Lautz says. Last week, when rates averaged 6.64%, home buyers could have paid about $70 less per month—but that was based on a median home price of $391,700.

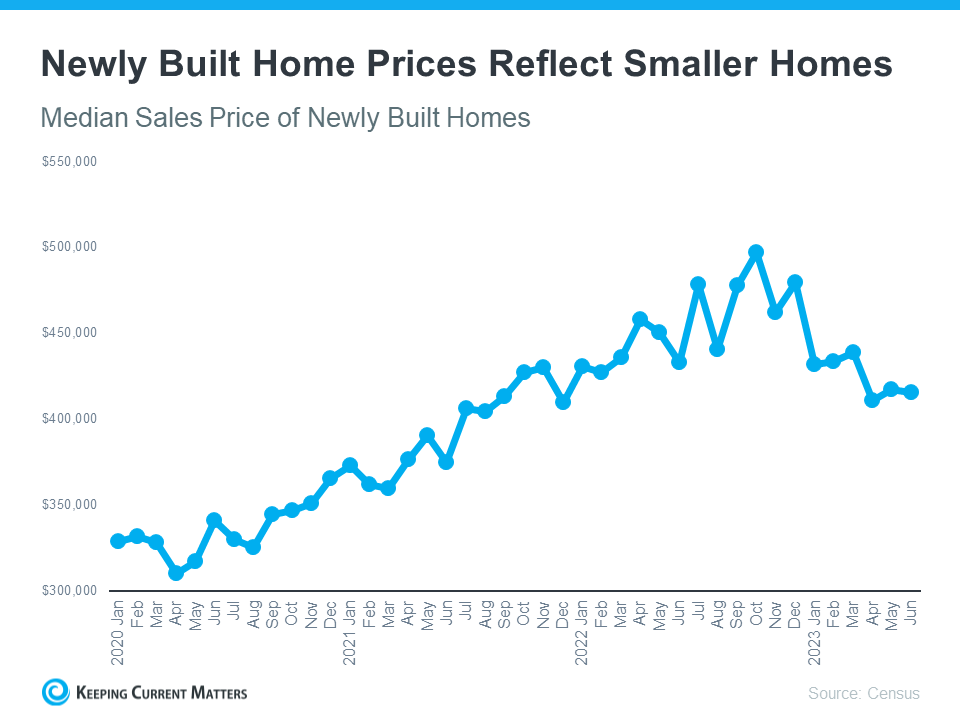

Home prices are rising quickly. The median price of an existing home surged to an all-time high in December, according to NAR, and prices are expected to continue to climb. The annual median home price is predicted to increase by 1.4% this year, and by another 2.6% in 2025, to $405,200, NAR’s forecast shows. Plus, housing inventory remains at historical lows and remain a major obstacle for would-be home buyers. That will keep pressure on home prices, economists say.

Freddie Mac reports the following national averages for mortgage rates for the week ending Feb. 15:

- 30-year fixed-rate mortgages: averaged 6.77%, rising from last week’s 6.64% average. Last year at this time, 30-year rate averaged 6.32%.

- 15-year fixed-rate mortgages: averaged 6.12%, up from last week’s 5.90% average. A year ago, 15-year rates averaged 5.51%.

Melissa Dittmann Tracey is a contributing editor for REALTOR® Magazine, editor of the Styled, Staged & Sold blog, and produces a segment called “Hot or Not?(link is external)” in home design that airs on NAR’s Real Estate Today radio show. Follow Melissa on Instagram and Twitter at @housingmuse.