Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

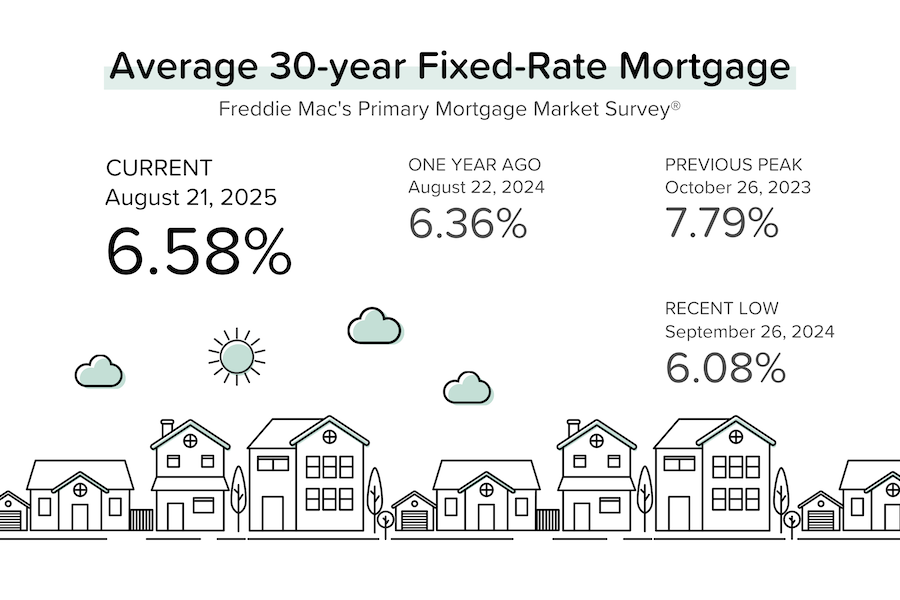

Mortgage rates ticked up slightly this week as the Federal Reserve hinted it may hold off on cutting rates in September. Even with the uncertainty, the 30-year fixed average is still hovering near 6.5%. At the same time, home prices are showing signs of softening nationwide, while builders are slowing new projects.

So what does all this mean if you’re a buyer or seller in today’s market? Let’s break it down.

What This Means for Buyers

If you’re looking to buy, the news is mixed but leans in your favor. Home prices fell in 39 of the 50 largest metro areas in July. Nationally, prices dipped only 0.1% month-over-month, but this was the third month in a row of small declines. Some of the biggest drops are happening in markets that saw the fastest price growth during the pandemic.

For buyers, that means there are more opportunities to negotiate—especially if a home has been sitting on the market. Rates near 6.5% aren’t as low as a few years ago, but they’re also steadier now, giving you a clearer picture for budgeting. For example, on a $300,000 loan, the difference between a 6.5% and 7% rate is about $100 a month. Stability matters.

Rental growth is also cooling, which takes some pressure off buyers who are weighing the rent-vs-buy decision. In cities like Dallas, rents are flat, while they’re even dropping in places like Phoenix and Denver.

What This Means for Sellers

Sellers face a more competitive landscape. With more homes on the market and buyers feeling cautious, pricing right is critical. Overpricing could mean your home sits, especially in areas where supply is climbing.

The good news? Even with prices easing, values are still higher than they were a year ago in many regions, especially the Northeast and Midwest. If you’ve owned your home for more than a couple of years, chances are you still have strong equity.

One key takeaway: buyers today are watching affordability closely. Homes that are move-in ready and priced realistically will draw more attention than ever.

Looking Ahead

The Fed’s decisions on interest rates will keep influencing mortgage costs. While most expect at least one rate cut before the end of the year, timing is still uncertain. Builders are also slowing down on new projects, which means supply may stay tight over the long term.

Whether you’re buying your first home or planning to sell, this market calls for strategy and flexibility.

Thinking about your next move? Let’s make a smart plan. Schedule a time at rob-hurt.com.