Buying a home is one of the most significant financial decisions many people will make in their lifetime, and for most people, a home mortgage is necessary to finance the purchase of a home. Mortgage payments, however, can be a significant financial burden, especially when you consider the interest you’ll be paying over the life of the loan. One way to reduce the interest you’ll pay is by buying discount points.

So, what are discount points, and how can they help you save money on your home mortgage?

Discount points are fees paid to your lender at closing that reduce the interest rate on your mortgage loan. Each point typically costs 1% of the total loan amount, and usually lowers the interest rate on your mortgage by 0.25%. For example, if you have a $200,000 mortgage loan, one discount point would cost you $2,000, and it could lower your interest rate by 0.25%.

Buying discount points can be an excellent option for those who plan to stay in their home for an extended period. The amount of interest you save each month can add up over time and save you a significant amount of money over the life of the loan.

However, before you decide to buy discount points, you should consider the following factors:

Your financial situation: Do you have the cash available to pay for discount points at closing? If not, it may not be worth it to buy discount points. (Pro Tip: A good Realtor can help you find a property/seller who might be willing to offer money at closing to help cover your closing cost…money which could be used to purchase discount points.)

How long you plan to stay in your home: If you plan to sell your home within a few years, buying discount points may not be worth it because you won’t have enough time to recoup the cost of the points.

The interest rate: Is the interest rate on your mortgage already low? If so, buying discount points may not save you as much money. (In our May 2023 market, buying discount points makes financial sense.)

Buying discount points can be an excellent way to save money on your home mortgage, but it’s not the only tool available, and that is why I partner with a reputable lender like Cardinal Financial. Cardinal offers an array of products and has the knowledge to put YOU in the best possible position to buy a home. The loan officers I work with truly put the needs of my clients above profits, finding the best products for them, and that’s why I have chosen to partner with Cardinal Financial.

If you are thinking about buying a home or dream of purchasing your first home, message me today and let’s schedule a time to talk discount points and more. I would LOVE to help you move into your dream home…maybe sooner than you thought possible!

You’ll probably experience some trial and error as you learn to properly care for your new place. Here’s a basic home-maintenance checklist to help you get started.

Check gutters regularly to make sure they’re properly attached and clear of sticks and leaves. Also, confirm the flow of water from your gutters is away from your home to avoid damage to your foundation.

Test your smoke and carbon monoxide detectors monthly. Experts also recommend changing the batteries in these items as part of your routine when you change the clocks in the fall and spring.

Change HVAC filters in your home at intervals recommended by the system manufacturer, especially if you have allergies or pets. A dirty filter means an inefficient system.

Inspect trees on your property. A tree-service company can give you advice on how to care for your trees and identify weak limbs that should be cut.

Look for running toilets and dripping faucets. These small nuisances can add up to a large waste of water. You can often fix a toilet or faucet yourself.

Check the supply hose to your washing machine, which can leak and cause expensive damage.

Clean your dryer vent regularly. Note the dryer vent is not the lint trap (which should be cleaned often, too). Dryer vents push air outside the property through a duct, but can get filled with lint and become a fire hazard.

Clean around your refrigerator. Keeping the vents and coils underneath and behind your refrigerator free of dust helps its efficiency.

Mind the gaps. Do you have gaps or cracks around doors, windows, or where pipes and wires enter the structure? Replace weather stripping that’s missing or in disrepair and add caulk where needed. This will help you keep the house insulated and keep bugs and small creatures out.

Have a pest-control expert inspect your home, even if you don’t suspect signs of infestation.

As you can see, a lot of effort goes into maintaining your home, and these tips just scratch the surface. Ask your REALTOR® about other resources that can help you keep your home safe, efficient, and well-maintained.

—-

When I find an article I believe will be helpful to my friends and clients, I post it here on my blog. If you would like to read the article from the original source, you may find it here.

When you are planning to buy a home, it’s important to have a clear idea of the costs involved, both upfront and ongoing. Here are a few things you should keep in mind:

Down payment: You will need to save up for a down payment, which is a percentage of the home’s purchase price that you pay upfront. Downpayment amounts can vary depending on what type of financing you will be using. A common first-time home buyer loan is an FHA loan with a down payment of 3.5%. (Down payment assistance programs can help cover some of this cost.)

Closing costs: These are the fees and expenses that you need to pay at the time of closing when you finalize the purchase of the home. These costs can include things like appraisal fees, lawyer fees, title insurance, and taxes. On average, closing costs can range from 2% to 5% of the home’s purchase price and your agent can help you estimate this cost based on your home price and other factors.

Monthly mortgage payments: Once you have bought your home, you will have to make monthly mortgage payments, which will include both principal (the amount you borrowed) and interest (the cost of borrowing) as well as property taxes and homeowners insurance. You can use online mortgage calculators to estimate your monthly payments based on the purchase price, down payment, and interest rate. Again, your agent can help you estimate this cost.

Buying a home is a big financial commitment, and it’s important to plan carefully and budget accordingly. You should also consider talking to a financial advisor or a mortgage lender to get more information and guidance on the costs of homeownership.

As a first-time home buyer, it’s also important to understand that your credit score plays a critical role in determining your eligibility for a mortgage and the interest rate you may qualify for. Here are some steps you can take to prepare your credit for buying a home:

Check your credit report: Start by checking your credit report from the three major credit bureaus (Equifax, Experian, and TransUnion). Your real estate agent can show you where to get these reports and help you know what to look for/work on. Your agents should also be able to direct you to a reputable credit repair service as well if you need more serious work on your credit.

Pay down debt: High levels of debt can lower your credit score and make it harder to qualify for a mortgage. Try to pay down your credit card balances and other debts to improve your credit utilization ratio, which is the amount of credit you’re using compared to your total credit limit.

Avoid applying for new credit: Every time you apply for credit, it can have a temporary negative impact on your credit score. Avoid applying for new credit cards or loans while you’re preparing to buy a home.

Pay bills on time:Late payments can also lower your credit score, so make sure to pay all of your bills on time. Consider setting up automatic payments or reminders to help you stay on track.

Build up your credit history: If you’re new to credit or have a limited credit history, consider applying for a secured credit card or becoming an authorized user on someone else’s credit card to help build your credit history. Also get/keep a record of your on-time rental payment history.

Overall, it’s important to start preparing your credit well in advance of buying a home. By taking steps to improve your credit score and financial standing, you may be able to qualify for a better interest rate and save money over the life of your mortgage. Your real estate agent can be a great resource for more information on these topics.

FHA loans are a type of mortgage that is backed by the Federal Housing Administration (FHA). This means that if a borrower defaults on their loan, the FHA will cover the lender’s losses, which makes it less risky for lenders to offer these loans to borrowers.

FHA loans are popular among first-time homebuyers because they require a lower down payment than most conventional loans. In fact, borrowers can put down as little as 3.5% of the purchase price of the home. This makes it easier for people to become homeowners, even if they don’t have a lot of savings.

Another advantage of FHA loans is that they are more forgiving of credit issues than some other types of loans. Borrowers with lower credit scores may still be able to qualify for an FHA loan, whereas they might not be approved for a conventional loan.

However, there are some limitations to FHA loans. There are maximum loan limits based on the area where the property is located, and borrowers may have to pay mortgage insurance premiums for the life of the loan. Additionally, the property being purchased must meet certain minimum property standards to be eligible for an FHA loan. (Click here to see FHA home appraisal checklist).

Overall, FHA loans can be a great option for homebuyers who need a more flexible mortgage option, but it’s important to work with a knowledgeable real estate agent and lender to determine if an FHA loan is the right choice for your specific situation. Let’s talk about your situation and find the best solution for you. #ICanHelp

Be very careful…what you don’t know could damage your property!

The law of unintended consequences, which applies to life in general, applies to landscaping in particular. In other words, planting over here could mean trouble over there.

We’ve delivered over 1 million home inspections over the last 30+ years – here are some simple landscaping do’s and don’ts that we’ve compiled from our inspection data.

Do: Plan ahead.

Golden eunoymus planted everywhere?

Planting is like life – planning for anything is always the preferable approach. If your landscaping dreams include planting new trees or shrubs near to your house, planning ahead is especially important.

Plants, shrubs, and trees are lovely additions to your property, but be aware that every plant and tree is different and has different needs in order to thrive. Most importantly, every plant has unique requirements for space, including room to grow.

Don’t: Plant shrubs too close to the house.

Is this shrub too close? (Yes.)

Avoid planting shrubs too close to your home, not just because plants will come into contact with and damage the siding, but because shrubs retain moisture.

Moisture deteriorates exterior cladding – The single biggest issue with regards to shrubbery growing near or on the structure is moisture, which will accelerate deterioration of practically any type of exterior cladding.

Moisture attracts termites – Moisture is the #1 “conducive condition” for termite infestations. Plants are organic “cellulose-based” organisms. Guess what termites eat? Cellulose-based organisms. While termites are mostly interested in dead wood (building materials), termites can also attack roots of live shrubs and trees. Therefore, whenever you plant anything close to the structure, you must consider the possibility that you may be planting termite food right next to your house. Termites are migratory – if they attack trees or shrubs near your house, guess where they’re headed next?

Is this shrub too close? (Yes.)

Baby shrubs grow into monster shrubs. What claims to be a dwarf shrub or mini crepe myrtle today could be a shade tree in the blink of an eye.

You’ve seen them – houses covered with what once were baby shrubs. You need to account for adult sizes when choosing a location on your property. And don’t believe the plastic tags. If a vendor claims that a shrub will be 24″ tall, expect it to grow to be twice that size.

If shrubs grow more than you initially anticipated, trim the shrubs regularly – there should be at least 1′ of space between shrubs and the exterior of the structure.

Do: Check your slope.

“Grading” describes surface elevation changes when compared to other areas around or near the house. Proper grading is when the grade or slope of the elevation slopes downward and away from the home at a rate of 1″ per foot for the first 6′ and then a continued slope for at least 10′ from the foundation.

Swales help to keep water flowing away from your house.

If the elevation looks flat or worse, slopes back towards the house, you have work to do before planting new anythings.

Grading should also ensure that water flows away from the house; if the grading near the house is OK but there’s a flood in the yard every time it rains, even the best near-home grading won’t prevent water intrusion.

Don’t: Plant trees too close to the house.

Why there’s water in the basement.

As bad as it is to plant shrubs too close to the house, you’re risking disaster if you plant trees too close to the house.

Why there’s no water at all.

Structural damage – Tree roots can cause structural damage to your home depending on the proximity and type of tree. Ficus trees, for example, have very aggressive root systems and even a small ficus tree planted close to a structure could cause foundation damage. Oaks and maples have massive root systems, but actually may cause less damage because their roots generally go around obstructions rather than through them.

Plumbing damage – Tree roots can also sometimes cause plumbing problems. Aggressive root systems bore through older, brittle plumbing components like cast iron and clay that are under the structure; large roots can actually crush plumbing components. Our Sewer Scope Inspection often reveals infiltration of root systems blocking drainage in municipal systems as well as septic systems, repairs of which can be very costly.

Roofing damage – Tree limbs which stretch over your house are accidents waiting to happen. But even if that old walnut tree stays upright for 100 years, contact with branches and debris from the leaves and small sticks will gradually and prematurely wear away your roof covering.

Heaving damage – Tree roots can damage walkways and driveways. Root systems that heave walkways and driveways not only cause concrete and asphalt damage, but also create a “trip hazard” due to uneven surfaces.

Give trees 15′ to 20′ space from the structure.

Talk to your local nursery professional if you want to learn more about the various root systems. Or check out The Right Tree in the Right Place at the Arbor Day Foundation.

Do: Ensure proper drainage.

Pretty wall, zero drainage, wet basement.

The best way to avoid structural deterioration from water is to keep the dwelling dry. Landscaping is an important component to help achieve a dry house. Planting according to area-specific types and species will help to ensure that excess water will be soaked up by plants, shrubs, trees, and lawn. Properties with poorly maintained landscaping are more susceptible to water penetration issues.

Installing barriers (retaining walls, landscaping timbers, vertical plastic edging, stones) can exacerbate the problem because barriers don’t just hold flowers and mulch – barriers block drainage. If you prefer to use landscape timbers and edging, make sure downspouts extend beyond the barriers. If your home is in cold climes, don’t direct downspouts onto the driveway and/or sidewalks; snow and freezing rain can make the walking areas unsafe and help to accelerate cracks in the driveway and/or sidewalk.

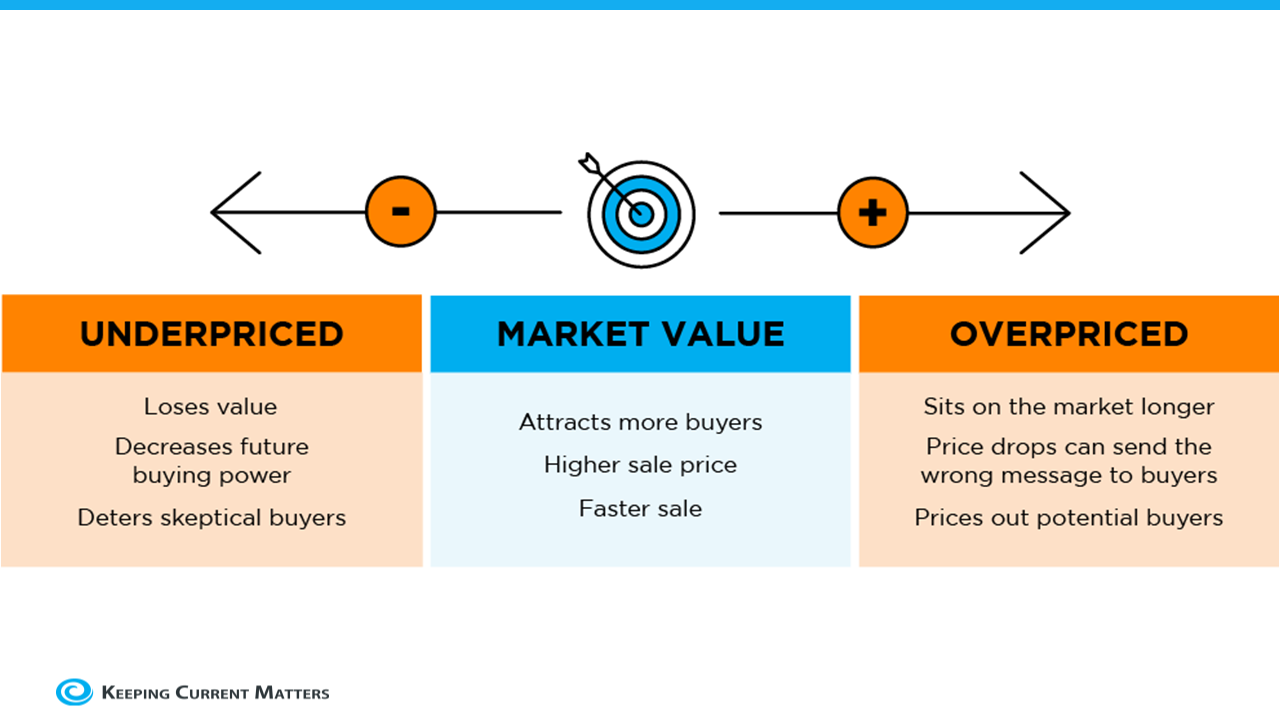

Over the last year, the housing market’s gone through significant change. While it’s still a sellers’ market, homes that are priced right are selling, and they get the most attention from buyers right now. If you’re thinking of selling your house this spring, it’s important to lean on your expert real estate advisor when it comes to setting a list price. As Realtor.comexplains:

“Move-in-ready homes with curb appeal and in desirable areas—and that are priced to sell—are especially likely to move quickly this spring.”

In today’s market, how you price your house will not only make a big difference to your bottom line, but to how quickly your house will sell.

Why Pricing Your House Right Matters

Your asking price sends a message to potential buyers, especially today. If it’s priced too low, you may leave money on the table or discourage buyers who may see a lower-than-expected price tag and wonder if that means something is wrong with the home.

If it’s priced too high, you run the risk of deterring buyers.When that happens, you may have to lower the price to drive interest when your house sits on the market for a while. But be aware that a price drop can be seen as a red flag by some buyers who will wonder what it means about the home.

To avoid either headache, price it right from the start. A real estate professional knows how to determine the ideal asking price. They balance the value of homes in your neighborhood, current market trends, buyer demand, the condition of your house, and more to find the right price. This helps lead to stronger offers and a greater likelihood your house will sell quickly.

The visual below helps summarize the impact your asking price can have:

Bottom Line

Homes priced at the current market value are selling faster, at a better price, and with less hassle right now. To make sure you price your house appropriately, maximize your sales potential, and minimize your hassle, reach out to a trusted real estate professional.

—-

When I find an article I believe will be helpful to my friends and clients, I post it here on my blog. If you would like to read the article from the original source, you may find it here.

Thinking about selling your house? If you’ve been waiting for the right time, it could be now while the supply of homes for sale is so low. HousingWire shares:

“. . . the big question is whether we are finally starting to see the seasonal spring increase in inventory. The answer is no, because active listings fell to a new low last week for 2023 . . .”

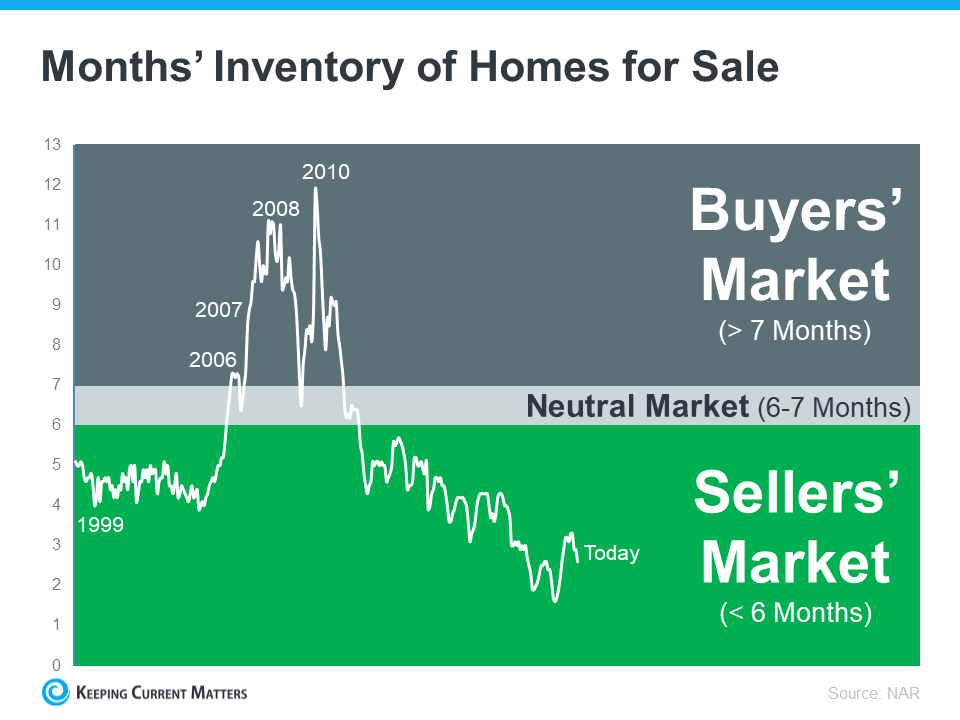

The National Association of Realtors (NAR) confirms today’s housing inventory is low by looking at the months’ supply of homes on the market. In a balanced market, about a six-month supply is needed. Anything lower is a sellers’ market. And today, the number is much lower:

“Total housing inventory registered at the end of February was 980,000 units, identical to January and up 15.3% from one year ago (850,000). Unsold inventory sits at a 2.6-month supply at the current sales pace, down 10.3% from January but up from 1.7 months in February 2022.”

Why Does Low Inventory Make It a Good Time To Sell?

The less inventory there is on the market when you sell, the less competition you’re likely to face from other sellers. That means your house will get more attention from the buyers looking for a home this spring. And since there are significantly more buyers in the market than there are homes for sale, you could even receive more than one offer on your house. Multiple offers are on the rise again (see graph below):

If you get more than one offer on your house, it becomes a bidding war between buyers – and that means you have greater leverage to sell on your terms. But if you want to maximize the opportunity for a bidding war to spark, be sure to lean on your expert real estate advisor. While we’re still in a strong sellers’ market, it isn’t the frenzy we saw a couple of years ago, and today’s buyers are focused on the houses with the greatest appeal. Clare Trapasso, Executive News Editor at Realtor.com, explains:

“Well-priced, move-in ready homes with curb appeal in desirable areas are still receiving multiple offers and selling for over the asking price in many parts of the country. So, this spring, it’s especially important for sellers to make their homes as attractive as possible to appeal to as many buyers as possible.”

Bottom Line

If you’ve been waiting for the right time to sell your house, low inventory this spring sets you up with a big advantage. Reach out to a local real estate professional today to make sure your house is ready to sell.

—-

When I find an article I believe will be helpful to my friends and clients, I post it here on my blog. If you would like to read the article from the original source, you may find it here.

Buying your dream home is simple with the right information, proper tools and a trusted real estate professional.

It’s no wonder that “91% of homeowners say they feel secure, stable or successful owning a home,” according to Unison. Buying your dream home is simple with the right information, proper tools and a trusted real estate professional.

Maintaining the latest news and trends is essential because data changes constantly. Knock forecasted that Dallas/Fort Worth would be among the 10 top markets with the most buyers’ options in 2023. This means that with more inventory for buyers, we will start to see the market shift. If you want to find your dream home, now is the perfect time to begin your search.

The home buyers’ guide starts with determining your budget and ends with closing, but there are many technical stops in between. The typical home buying process has not seen innovation in quite some time, so we decided to change that. CENTURY 21 Judge Fite Company is here to guide you on the road to home ownership so that you can focus on the things that matter most.

Our one team approach is one you won’t find anywhere else. From the agent, title company, mortgage lender, insurance, property management and vendor connections, we steer you right from the start for a lifetime. No need to scour the internet for millions of articles, reviews, and listings because we have it all in one place.

Ready to begin the road to homeownership? Let’s find your dream home today!

—-

When I find an article I believe will be helpful to my friends and clients, I post it here on my blog. If you would like to read the article from the original source, you may find it here.

Follow C21JFC on Facebook, Instagram and LinkedIn to keep up with the latest home tips, real estate news and resources across DFW. Subscribe to our monthly newsletter, Real Estate 411 here.

Spring has arrived, and that means more and more people are getting their homes ready to sell. But with recent shifts in real estate, this year’s spring housing market will be different from the frenzy of the past several years. To sell your house quickly, without hassles, and for the most money, be sure to follow these four simple tips:

1. Make Sure You Give Buyers Access

One of the biggest mistakes you can make as a seller is limiting the days and times when buyers have access to view your home. In any market, if you want to maximize the sale of your house, you can’t limit potential buyers’ access to view it. If it’s not accessible, it could cost you by sitting on the market longer and ultimately selling for a lower price.

2. Make Your Home Look as Good as Possible on the Inside

For anything to sell, especially your home, it must look inviting. Your real estate agent can give you expert advice on ideal staging for your home. Even updating a room with fresh paint, steam cleaning carpets, or removing clutter from the garage can make a big impact.

3. First Impressions Matter

The old saying “you never get a second chance to make a first impression” matters when selling your house. Often, the first impression a buyer gets is what they see as they walk up to the front door. Putting in the work in on the exterior of your home is just as important as what you stage inside. Freshen up your landscaping to improve your home’s curb appeal so you can make an impact with potential buyers.

4. Price It Right

This is probably the most important aspect of selling your home in today’s real estate market. If a house is priced competitively, it’s going to sell. Period. To do this, you have to know what’s happening with home prices in your area and understand the factors that are affecting the market right now. That’s why it’s best to work with a trusted real estate professional who can ensure you list your house at the right price.

Bottom Line

Everyone selling their home wants three things: to sell it for the most money they can, to do it in a certain amount of time, and to do all of that with the fewest hassles. To accomplish these goals, start by connecting with a local real estate professional to understand the steps you need to take to sell your home this spring.

—-

When I find an article I believe will be helpful to my friends and clients, I post it here on my blog. If you would like to read the article from the original source,you may find it here.

Even though activity in the housing market has slowed from the frenzy we saw over a year ago, today’s low supply of homes for sale is still a sellers’ market. But what does that really mean? And why are conditions today so good if you want to list your house?

It starts with the number of homes available for sale. The latest Existing Home Sales Reportfrom the National Association of Realtors (NAR) shows housing supply is still astonishingly low. In Arlington today, we have a 1.4-month supply of homes at the current sales pace. Historically, a 6-month supply is necessary for a ‘normal’ or ‘neutral’ market in which there are enough homes available for active buyers (see graph below):

What Does This Mean for You?

When the supply of homes for sale is as low as it is right now, it’s much harder for buyers to find one to purchase. That creates increased competition among purchasers and keeps upward pressure on prices. And if buyers know they’re not the only one interested in a home, they’re going to do their best to submit a very attractive offer. As this happens, sellers are positioned to negotiate deals that meet their ideal terms. Lawrence Yun, Chief Economist at NAR, says:

“Inventory levels are still at historic lows. Consequently, multiple offers are returning on a good number of properties.”

Right now, there are still buyers who are ready, willing, and able to purchase a home. If you list your house right now in good condition and at the right price, it could get a lot of attention from competitive buyers.

Bottom Line

Today’s sellers’ market can be a great time for homeowners ready to make a move. Listing your house now will maximize your exposure to serious, competitive buyers. Connect with a local real estate professional to jumpstart the selling process.

—-

When I find an article I believe will be helpful to my friends and clients, I post it here on my blog. If you would like to read the article from the original source,you may find it here.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link